The following questions and answers are intended to guide shipping professionals in understanding the application of the EU Emissions Trading System to maritime transport. They do not replace the legislation. For further detail, please consult the updated EU Emissions Trading System Directive. The content was last updated 08/02/2024.

The EU Emissions Trading System (EU ETS) will be extended to maritime transport emissions from 2024.

The new rules entered into force on 5 June 2023.

The EU Emissions Trading System, together with the monitoring, reporting and verification (MRV) of ships’ emissions, are one of the Commission’s main tools to reduce greenhouse gas emissions in maritime transport.

For instance, they concern the administration of shipping companies by administering authorities, the creation of maritime accounts in the Union Registry, specific rules in relation to monitoring, reporting and verification.

For more details on the state of play of adoption of these acts, please refer to the section ‘Legislative Process’ on CLIMA’s maritime webpage.

To prepare these acts, the Commission is assisted by a maritime formation within the existing Expert Group on Climate Change Policy (CCEG), involving experts from EU Member States. In addition, there are other consultation activities, also involving the industry through the European Sustainable Shipping Forum (ESSF). These acts are also prepared with the support of the European Maritime Safety Agency (EMSA).

The MRV Maritime Regulation and ETS Directive apply to Norway and Iceland. The texts have been incorporated into the EEA Agreement (Annex XX).

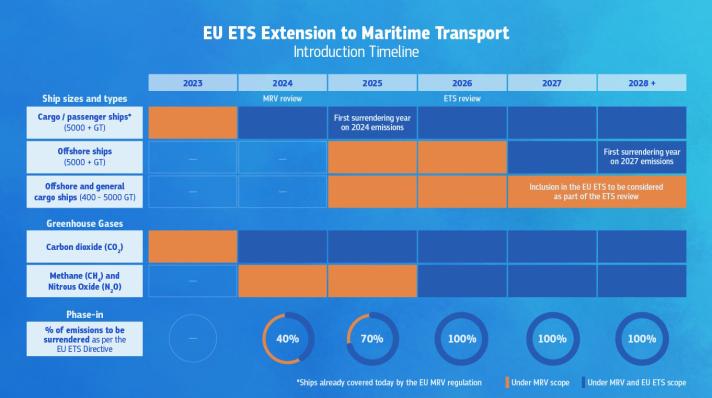

Shipping companies must surrender (use) their first ETS allowances by 30 September 2025 for emissions reported in 2024.

The share of emissions that must be covered by allowances gradually increases each year:

- 2025: 40% of emissions reported for 2024 must be covered by emission allowances

- 2026: 70% of emissions reported for 2025

- 2027 and beyond: 100% of reported emissions

- From 2024: cargo and passenger ships of or above 5000 gross tonnage (GT)

- From 2027: offshore ships of or above 5000 GT

As of 1 January 2025, companies must report emissions for the following ships:

- Cargo and passenger ships of or above 5000 GT;

- Offshore ships of or above 5000 GT;

- Offshore ships and general cargo ships below 5000 GT but not below 400 GT.

The EU MRV Maritime Regulation covers:

- Carbon dioxide (CO2)

- Methane (CH4) as of 2024

- Nitrous oxide (N2O) as of 2024

The EU ETS covers:

- Carbon dioxide (CO2)

- Methane (CH4) as of 2026

- Nitrous oxide (N20) as of 2026

The system is flag-neutral and route-based. This means it covers emissions from maritime transport as follows:

- 100% of emissions from ships performing voyages departing from a port under the jurisdiction of an EU Member State [see question on EEA countries above for more information] and arriving at a port under the jurisdiction of an EU Member State (e.g. Hamburg to Marseille and Marseille to Hamburg);

- 100% of emissions from ships within a port under the jurisdiction of an EU Member State (e.g. in the port of Antwerp), i.e. emissions released at berth and during movements within such a port;

- 50% of emissions from ships performing voyages departing from a port under the jurisdiction of an EU Member State and arriving at a port outside its jurisdiction (e.g. Rotterdam to Shanghai);

- 50% of the emissions from ships performing voyages departing from a port outside the jurisdiction of an EU Member State and arriving at a port under the jurisdiction of an EU Member State (e.g. Shanghai to Rotterdam).

Some derogations will apply, for instance for certain voyages to outermost regions or some small islands, or to the benefit of ships using renewable fuels. [see sections on ‘Specific rules and derogations’ and ‘Biofuels and other alternative fuels’ below for more information].

A port of call is the port where a ship stops to load or unload cargo, to embark or disembark passengers, or where an offshore ship stops to relieve the crew. The following stops are excluded:

- stops for the sole purposes of refuelling,

- stops for obtaining supplies,

- stops for relieving the crew (other than an offshore ship),

- stops for going into dry-dock or making repairs to the ship and/or its equipment,

- stops in port because the ship is in need of assistance or in distress,

- ship-to-ship transfers carried out outside ports,

- stops for the sole purpose of taking shelter from adverse weather or rendered necessary by search and rescue activities,

- stops of containerships in the neighbouring container transhipment ports listed in the corresponding implementing act.

The surrendering requirements as per the ETS Directive apply to emissions within a port of call under the jurisdiction of a Member State. Such emissions result from the sum of emissions at berth and emissions within a port of call while not at berth, i.e., emissions from movements in a port under the jurisdiction of a Member State.

It is to be noted that emissions related to the entry into or exit from ports that take place before or after the port of call are part of the voyage; they are not to be considered as ‘emissions within ports’.

Emissions at berth correspond to emissions when a ship is securely moored or anchored in a port falling under the jurisdiction of a Member State while it is loading, unloading or hoteling, including the time spent when not engaged in cargo operations.

Emissions within ports encompass the entirety of emissions within a port of call under the jurisdiction of a Member State, meaning that both emissions from activities while at berth and emissions while within port but not at berth (i.e., emissions from movements within the port) are to be accounted for. The latter are to be understood as emissions taking place within port limits but only when not already included in a voyage.

A reporting period is the period from 1 January until 31 December of any given calendar year. Hence, for voyages starting and ending in two different calendar years, the respective data must be accounted under each reporting period. Following the example above, this means that the amount of emissions until 31 December 2024, as monitored by the shipping company, will be reported as part of the 2024 emissions report, while the amount of emissions corresponding to the part of the voyage as of 1 January 2025 will be accounted for in the 2025 emissions report.

No. Shipping companies will need to surrender (use) EU allowances (EUA) corresponding to the amount of aggregated emissions data at company level to be reported under the EU ETS Directive. Carbon credits or certificates cannot be used for EU ETS compliance purposes.

For instance, an implementing act lays down the new templates for monitoring plans, emissions reports and reports at company level. You may find more information on the latest state of play under the ‘Legislative process’ section of CLIMA’s maritime webpage.

The EU Emissions Trading System (ETS) is a ‘cap-and-trade’ system. A cap is a threshold, defining the total amount of greenhouse gases that can be emitted by the operators covered by the system. It is reduced annually, at fixed intervals, in line with the EU’s climate target.

The ETS objective is to reduce emissions by 62% from 2005 to 2030.

The cap is expressed in emission allowances, where one allowance gives the right to emit one tonne of CO2eq (carbon dioxide equivalent). Operators are not allowed to generate more greenhouse gas emissions than their allowances can cover. If they do, heavy fines are imposed. Companies covered by the EU ETS must surrender (use) EU allowances corresponding to their emissions in the Union Registry. For instance, if a company emits 10,000 tonnes of CO2 falling within the scope of the EU ETS Directive during a reporting period, that company needs to buy and surrender 10,000 allowances by 30 September of the following year. Emission allowances are auctioned, and companies can buy and sell them through secondary markets.

The system allows flexibility for companies to cut their emissions in the most cost-effective way. Indeed, every year, companies are incentivised to reduce their emissions or to continue to pay for those emissions (i.e. to surrender the corresponding amount of allowances).

Shipping companies covered by the EU ETS are required to have an approved monitoring plan for monitoring and reporting annual emissions. Every year, companies must submit an emissions report for each of the ship under their responsibility, as well an emissions report at company level (aggregating the ship data to be reported for ETS purposes). The data for a given year must be verified by an accredited verifier by 31 March of the following year (or by 28 February if so requested by the administering authority). Once verified, companies must surrender (use) the equivalent number of allowances by 30 September of that year.

Shipping companies are subject to obligations under the MRV Regulation since 2018. Data must be reported through THETIS-MRV, a platform operated by the European Maritime Safety Agency (EMSA) which enables, among other benefits, the publication of reliable data on ships’ emissions.

Please find more information in the FAQ on the MRV Maritime Regulation.

Yes, shipping companies must continue reporting their greenhouse gas emissions through the existing THETIS-MRV platform. The latter will be updated in order to reflect the changes made by the revised MRV Maritime Regulation and ETS Directive. On the basis of the reported aggregated emissions data at company level, companies will then be required to surrender (use) a corresponding amount of EU allowances in the Union Registry.

The rules on the Union Registry are currently being revised, notably with a view to reflecting the inclusion of the maritime sector within the EU ETS (e.g., through the creation of new ‘Maritime Operator Holding Accounts’- MOHA). The revised act has been adopted by the Commission in the end of October and is submitted to the European Parliament and Council for scrutiny until 25 December 2023. Provided that these institutions do not raise any objections within two months, the act will be published in the Official Journal of the EU and will enter into force by the end of 2023. The draft act is accessible here.

According to the draft revised Registry Regulation, under scrutiny by the European Parliament and the Council until 25 December 2023, a shipping company shall submit to the relevant national administrator the information to request the opening of a Maritime Operator Holding Account:

- within 40 working days of the publication of the attribution list (to be published by the Commission by 1 February 2024);

- for shipping companies not included in that list, within 65 working days of the first port of call falling within the scope of the ETS Directive.

No. Shipping companies will need to acquire general EU allowances (EUA), the same ones used by industry, power sector and aircraft operators.

Shipping companies will need to surrender allowances in the EU Member State corresponding to their administering authority. For this purpose, shipping companies will need to open a Maritime Operator Holding Account in that EU Member State.

[see questions on ‘Administering authorities’ for more information about the rules to associate companies with the administering authority of one EU Member State]

Emission allowances can be purchased in the primary market through auctions on the European Energy Exchange (EEX), which is currently contracted by the EU and its EU Member States to manage this system. There is also a secondary market in which allowances can be sold bilaterally or through various derivatives provided by financial institutions. To purchase ETS allowances, companies need to open a trading account or a maritime operator holding account in the Union Registry. Please note that the latter option will not be available before 2024.

Shipping companies may buy EU allowances already now notably on the secondary market, e.g, through derivative contracts.

According to the provisions of the Union Registry Regulation on the opening of a trading account, a shipping company could request the opening of such account to a national administrator provided that it fulfills the conditions and provides all the necessary information, as required by the national administrator.

Please note that a shipping company has no obligation to request the opening of a trading account.

The process for opening trading accounts takes place online and is open to non-EU citizens, subject to conditions spelled out by each EU Member State (through their National Administrator). Users must first open an account in the Union Registry to be able to trade EU allowances.

EU allowances (EUA) issued on or after 2013 do not expire and may be banked for future years. However, an allowance that has been surrendered cannot be retrieved.

Please see our webpage on the Union Registry

The shipping company is defined as ‘the shipowner or any other organisation or person, such as the manager or the bareboat charterer, that has assumed the responsibility for the operation of the ship from the shipowner and that, on assuming such responsibility, has agreed to take over all the duties and responsibilities imposed by the International Management Code for the Safe Operation of Ships and for Pollution Prevention, set out in Annex I to Regulation (EC) No 336/2006 of the European Parliament and of the Council.’

In the context of ETS and MRV, this means that the entity responsible for compliance in respect of the emissions of a given ship can be either the shipowner (i.e., the registered owner) or the ISM Company of that ship. The registered owner and the ISM Company have to decide who is the most appropriate entity to take on responsibilities for complying with the ETS and MRV obligations. In the absence of an explicit decision by the registered owner and the ISM Company, the registered owner will be considered, by default, responsible for compliance with ETS and MRV obligations.

In accordance with the Implementing Regulation (EU) 2023/2599, shipping companies must share information on the ship(s) for which they assume responsibility with their administering authority.

If the registered owner decides to assume responsibility for ETS and MRV obligations, the registered owner must provide the administering authority with a document listing the ship(s) for which the registered owner assumes responsibility.

If the ISM Company agrees to assume responsibility for ETS and MRV obligations in respect of one or several ships, the ISM Company must provide the administering authority responsible with a document that demonstrates the existence of an agreement according to which the ISM Company is mandated by the registered owner to comply with ETS and MRV obligations in respect of one or several ships.

In the absence of such a document, the registered owner is considered the entity responsible for compliance with ETS and MRV obligations, by default.

The ISM Company that assumes ETS and MRV responsibilities in respect of a given ship must also provide to its verifier the document demonstrating the mandate between the registered owner and the ISM Company, as part of the documents accompanying the monitoring plan of the ship.

The shipping company always remains the responsible entity for surrendering allowances.

The term ‘registered owner’ refers to the owner specified on a ship’s certificate of registry. The registered owner is assigned an IMO Unique Company and Registered Owner Identification Number.

Please note that, in respect of a given ship, a bareboat charterer cannot be considered as the shipowner within the meaning of the ETS Directive. This consideration also applies in the case where the ship is subject to a ‘parallel registration’ in the registry of two administrations.

The bareboat charterer can be responsible for compliance with ETS and MRV in respect of a given ship only if that bareboat charterer has accepted to assume ISM Code responsibilities in respect of that ship.

That bareboat charterer that assumes ISM Code responsibilities could accept to assume the responsibilities for ETS and MRV obligations from the registered owner. In such a case, the ISM Company must provide evidence of the mandate from the registered owner to its administering authority (see reply to “Who is responsible for complying with the obligations under MRV and ETS?”).

A bareboat charterer cannot be considered as the shipowner under ETS and MRV. Like in other matters, a shipowner may ask a third party to fulfil tasks on its behalf, including concluding contracts. Therefore, a bareboat charterer could sign a mandate with an ISM company on behalf of the registered owner if the bareboat charterer has been empowered to fulfil that task by the registered owner.

Yes, the entity responsible for compliance with the ETS obligations shall also be responsible for compliance with MRV obligations, in line with the definition of ‘company’ in the MRV Regulation and in the Recital 10 of Regulation (EU) 2023/957.

As an example, the shipowner that assumes responsibilities for ETS obligations is also responsible for compliance with MRV obligations. In practice, the shipowner might decide to delegate some operational tasks (e.g., data collection and monitoring) to another entity, for instance a ship manager. In that example, and despite this delegation of tasks, Member States will consider the shipowner as the sole entity responsible for compliance with ETS and MRV obligations.

In case the responsibility for the purchase of the fuel and/or the operation of the ship is assumed by an entity other than the shipping company pursuant to a contractual arrangement, the shipping company is entitled to reimbursement from that entity for the costs arising from the surrendering of allowances. EU Member States must take national measures to ensure that the shipping company is entitled to reimbursement in such situations and must provide the corresponding access to justice to enforce that entitlement.

Although this entitlement to reimbursement should be made effective by EU Member States regardless of contractual arrangements, shipping companies and entities responsible for the purchase of the fuel and/or the operation of the ship are expected to develop contractual clauses to pass on the ETS surrendering costs as appropriate. ‘Operation of the ship’ for the purposes of this provision means determining the cargo carried or the route and the speed of the ship.

Nevertheless, the shipping company remains the responsible entity for surrendering allowances.

Companies must, for each ship under their responsibility (at the end of the reporting period), submit an emissions report for the entire reporting period of the previous year, which has been verified as satisfactory by a verifier. This is true regardless of company changes and of who is responsible for surrendering allowances for these emissions [see the question below for more information on the surrendering]. The emissions report should cover the whole reporting period: for the period of the year during which the ship was under the responsibility of another company, the report would be based on the partial emissions report submitted by that previous company.

The shipping company is responsible for surrendering allowances corresponding to emissions from their ships during the time they were under their responsibility. This means that if there is a change of shipping company from Company A to Company B on 1 April 2025, then in 2026, Company A will need to surrender allowances corresponding to emissions from that ship from 1 January to 1 April 2025 [see Article 11(2) of the MRV Maritime Regulation for further details].

Each shipping company covered by the ETS has to be associated with the administering authority of one Member State.

A shipping company is associated to a Member State according to the attribution list published by the Commission on 31 January 2024. To ensure stability, a shipping company remains assigned to the Member State indicated in the list regardless of subsequent changes in the shipping company’s activities or changes in registration, until those variations are reflected in a new version of the list. Please note that the list will only be updated every two years (or every four years for non-EEA companies attributed to a Member State based on their ports of call in the last four monitoring years), in accordance with the rules laid down In Article 3gf(2) of the EU ETS Directive.

For new shipping companies not included in the attribution list but performing voyages covered by the EU ETS Directive, the rules spelled out in Article 3gf of the Directive apply (see the question below). Based on these rules, companies should therefore identify which is their administering authority via the THETIS-MRV system.

The THETIS-MRV helpdesk will help the companies assign their responsible administering authority in the system. The helpdesk may be contacted through the following email address: maritimesupportservices emsa [dot] europa [dot] eu (maritimesupportservices[at]emsa[dot]europa[dot]eu). Once associated with an administering authority, the company will then be added to the next update of the attribution list.

emsa [dot] europa [dot] eu (maritimesupportservices[at]emsa[dot]europa[dot]eu). Once associated with an administering authority, the company will then be added to the next update of the attribution list.

The rules to associate shipping companies to administering authorities are laid down in Article 3gf(1) of the EU ETS Directive, i.e.:

- In case of a shipping company registered in an EU Member State, it is the EU Member State where the shipping company is registered;

- In case of a shipping company not registered in an EU Member State, it is the EU Member State with the greatest estimated number of port calls from voyages performed by that shipping company over the last four monitoring years;

- In case of a shipping company that is not registered in an EU Member State and that did not carry out any voyage covered by the EU ETS Directive in the preceding four monitoring years, the administering authority is the EU Member State where a ship of the shipping company has arrived or has started its first voyage falling within the scope of the EU ETS Directive.

No. Not being on the attribution list does not exempt companies from ETS obligations. Any shipping company with ships doing voyages covered by the ETS during a reporting period shall comply with the relevant ETS obligations. If a shipping company is not on the list, it shall determine its administering authority in line with the ETS Directive (see the question above). To do so, the company should:

- create a user account in the THETIS-MRV system (if not already existing)

- add the new company to the user account

- follow the steps for attributing the new company to an administering authority (see the question below for more details).

The THETIS-MRV Helpdesk will be available assist the company in assigning its responsible administering authority in the system.

The company should then request the opening of a Maritime Operator Holding Account (MOHA) in the Registry and contact the relevant national administrator for this purpose.

On the other hand, an entity on the attribution list might not be subject to ETS obligations if it does not fulfil the conditions to be considered a ‘shipping company’ or if it does not have any active ship falling within ETS scope under its responsibility – despite being on the list due to past activities.

Firstly, the company should create a user account in THETIS-MRV (if not already existing) and add the new company to that account.

If established in an EEA country, according to the information recorded in THETIS-MRV, the company may already send a request to the THETIS-MRV Helpdesk to be assigned to the administering authority of that EEA country.

If established in a non-EEA country, according to the information recorded in THETIS-MRV, the company should:

- first, ensure that all the ships under its responsibility falling within ETS scope are assigned to its company account in THETIS-MRV

- only after, the company should send a request to the thetisemsa [dot] europa [dot] eu (THETIS-MRV Helpdesk) to be assigned to the administering authority of the EU Member State where the first port of call took place.

Please note that it is highly recommended to first finalise the submission of emissions reports for 2023 (or partial emissions reports for 2024) before releasing ships from their previous company to their new one in THETIS-MRV. This is because the previous company will not be able to submit an emissions report for a ship that is not in its fleet anymore, which could impact the issuance of the Document of Compliance.

The entities subject to EU ETS obligations are shipping companies. Therefore, EU Member States administer shipping companies, not individual ships.

Please note that the attribution list published by the Commission does not list ships, but only shipping companies. Once assigned to a Member State, a shipping company remains assigned to that Member State, at least until the next update of that list, regardless of subsequent changes in the company’s activities, e.g., ships entering or exiting their fleet.

Example: Under the EU ETS, the shipping company Alpha is responsible for two ships (Ship 1 and Ship 2). Alpha is attributed to Member State A. In January 2025, the responsibility for Ship 1 is transferred from shipping company Alpha to shipping company Beta, which is attributed to Member State B.

Such transfer of responsibility from Alpha to Beta concerning Ship 1 constitutes a change in the activities of Alpha and Beta, but this change has no impact on the respective attribution of Alpha and Beta to, respectively, Member State A and Member State B.

Until the 2026 update of the list, Alpha remains attributed to Member State A and Beta remains attributed to Member State B, independently of the transfer of Ship 1.

For the establishment of the list, the Commission, attributed each shipping company to a Member State with the support of the European Maritime Safety Agency. This was done in accordance with the rules laid down in the EU ETS Directive and in the Implementing Regulation (EU) 2023/2599. Information on the company’s registration was extracted from the data available in the THETIS-MRV system, while information on port calls’ history was obtained via the Union maritime information and exchange system established by Directive 2002/59/EC (‘SafeSeaNet’).

To establish the first attribution list in due time, this was done on 20 November 2023. The operation covered all the entities that had a company account with at least one ship registered in THETIS-MRV on that date.

Since the amended definition of ‘company’ in the MRV Maritime Regulation applies from 1 January 2024, some of the entities in this first attribution list may not fulfil the criteria of that new definition. Therefore, an entity appearing on the list is not necessarily subject to ETS obligations. Listed entities would only be subject to ETS obligations if they fulfil the conditions to be considered a ‘shipping company’ and if they have active ships falling within ETS scope under their responsibility.

Shipping companies mentioned in the attribution list published on 31 January 2024 should request the opening of a MOHA within 40 working days of the publication of the list.

Shipping companies that are not on the list should only request the opening of a MOHA once attributed to an EU Member State via the THETIS-MRV system. They must request the opening of a MOHA within 65 working days of the first voyage falling within ETS scope.

Please note that a list of contact points of national administrators (for Registry purposes) is available on our Union Registry webpage Shipping companies shall provide the required information in accordance with the amendments to the Registry Regulation.

No. To ensure stability, once assigned to an EU Member State, a shipping company remains assigned to that Member State regardless of subsequent changes in the shipping company’s activities or changes in registration, until those variations are reflected in an updated attribution list. The list will be updated every two years (or four years for non-EEA companies that were associated based on their historical ports of call in the last four monitoring years).

The attribution list was based on the best available information recorded by companies in the THETIS-MRV system and, as far as ports of call are concerned, as reported in SafeSeaNet.

Any requests for changes in the attribution to Member States will be disregarded.

Although companies will remain assigned to the Member State attributed to them until the release of an updated list, please note that ships may be transferred between companies, following the sale/purchase of a ship or simply a change of responsibility due to MRV and ETS compliance obligations, e.g. between a shipowner and an ISM company. Such cases will qualify as a change of company within the MRV Regulation. This means that the new company should submit a revised monitoring plan, whilethe previous one should submit a partial emissions report (in case the change of company occurs during a reporting period).

Ships’ emissions will be verified by verifiers accredited by EU Member States (i.e. National Accreditation Bodies). Shipping companies will be able to select any duly accredited verifier for each of their ships, irrespective of the ship's flag or the place where the company is based and where the accredited verifier is based. In principle, a company may have different verifiers for each of their ships, as well as different verifiers verifying the ship’s emissions report and the report at company level.

Member States will ensure that all shipping companies under their responsibility comply with the various obligations under the EU ETS. Member States will ensure that shipping companies under their responsibility surrender sufficient allowances in due time. Information about the compliance status of regulated entities will be derived from the Union Registry and be made accessible to the relevant authorities.

Shipping companies that fail to surrender allowances are liable to an excess emissions penalty of EUR 100 (corrected for inflation) per tonne of CO2 equivalent and are still liable for the surrender of the required allowances. The names of the penalized companies are also disclosed to the public.

EU Member States must set out penalties that are effective, proportionate, and dissuasive.

Furthermore, in case a shipping company has failed to comply with surrendering its obligations for two or more consecutive reporting periods, and where other enforcement measures have failed to ensure compliance, the competent authority of the EU Member State of the port of entry may, after giving the opportunity to the company concerned to submit its observations, issue an expulsion order. In practice, this means that every EU Member State is required to refuse entry to the ships under the responsibility of the shipping company concerned into any of its ports, until the company fulfils its surrendering obligations. Where a ship flies the flag of an EU Member State and enters or is found in one of its ports, the concerned EU Member State will, after giving the opportunity to the concerned company to submit its observations, detain the ship until the company fulfils its obligations.

The ETS Directive contains a detailed reporting and review clause specific to the inclusion of maritime transport in the EU ETS (Article 3gg of the ETS Directive.

For example, the Commission shall monitor the implementation of the ETS in relation to maritime transport. The Commission will closely monitor the possible risk of evasion and the impacts of the EU ETS on the overall competitiveness of the maritime sector in the Member States.

If appropriate, the Commission shall propose measures to ensure the effective implementation.

The revised EU ETS provides dedicated support to accelerate the decarbonisation of the maritime sector through the Innovation Fund. According to the Commission, 20 million allowances (i.e., about €1.6 billion with a price of €80 per allowance) should be deployed up to 2030 via the Innovation Fund to support the decarbonisation of the maritime sector, notably through dedicated topics in future calls for proposals. The Innovation Fund could support a wide diversity of projects and innovative solutions in the maritime sector, across the whole sector and at scale, including in relation to the production and uptake of renewable and low-carbon fuels.

Besides the Innovation Fund, all auction revenues attributed to EU Member States have to be used for climate-related purposes. The list of these purposes has been expanded to explicitly cover measures to decarbonise the maritime sector, including ports. The list also includes the financing of climate action in vulnerable third countries, including adaptation to the impacts of climate change.

Additional information on the Innovation Fund can be found here.

Emissions from all ships covered by the EU ETS are treated in the same way.

However, ships of ice class IA, IA Super or an equivalent ice class, established based on recommendation of the Baltic Marine Environment Protection Commission (HELCOM), may surrender 5% fewer allowances than their verified emissions released until 31 December 2030. The reason for the difference in treatment is that such ships, due to their design, require more fuel to cover the same distance when traveling in the open sea or under ice conditions. This derogation applies regardless of whether the concerned ship sailed in ice conditions during a reporting period.

Yes. Until 31 December 2030, shipping companies are not obliged to surrender allowances for emissions released by passenger ships, other than cruise passenger ships, and by ferries (ro-pax ships) during certain voyages between ports of certain islands of a Member State and ports located in the same Member State.

This derogation will only apply in respect of specific ports and islands that fulfil the conditions established in the ETS Directive, and upon request of the relevant Member State. For example, an eligible island must have a population of fewer than 200 000 permanent residents and must not have any road or rail link with the mainland.

The list of ports and islands concerned by that derogation has been published on 22 December 2023 in the Official Journal of the EU.

Please note that, in April 2024, three Finnish ports have been added to that list, via an amending Implementing Decision. The derogation also applies to those ports from 1 January 2024.

For easier convenience, you may refer to the consolidated list of all islands and ports concerned by that derogation.

Yes. Until 31 December 2030, shipping companies are not obliged to surrender allowances for emissions released from voyages between a port located in an outermost region of an EU Member State and a port located in the same EU Member State (e.g. Lanzarote-Valencia), including voyages between ports within an outermost region (e.g. Lanzarote-Fuerteventura) and voyages between ports in the outermost regions of the same EU Member State (Guadeloupe-Martinique). In addition, shipping companies are not obliged to surrender allowances in respect of emissions released within the ports in relation to such voyages.

In case of transnational public service obligations (or transnational public service contracts) established by two EU Member States, one having no land border with another EU Member State and the other being the closest, shipping companies are not obliged to surrender allowances for emissions released by passenger ships or ferries (ro-pax ships) operating under such a public service obligation or public service contract until 31 December 2030. The list of concerned public service contracts or obligations has been published on 22 December 2023 in the Official Journal of the EU. It is accessible here.

The obligation to monitor and report emissions as per Articles 3gd and 3ge of the ETS Directive and as per the EU MRV Maritime Regulation is still valid, even if all emissions from the ships under the company’s responsibility fall within the scope of a surrender derogation as provided for in Article 12(3-d) to (3-b) of the EU ETS Directive. These derogations have impacts only on the surrendering obligations.

Emissions of ships released from activities within a port in relation to voyages falling within the scope of a surrender derogation as provided for in Article 12(3-d) to 12(3-b) of the ETS Directive also benefit from the surrender derogation.

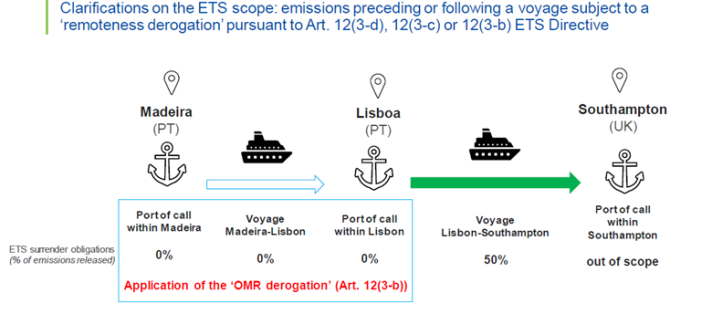

An illustration is provided below with regards to the derogation related to outermost regions (‘OMR derogation’). The emissions from the voyage from Madeira (port located in an outermost region of Portugal) to Lisbon (port located in ‘mainland’ Portugal) are subject to the surrender derogation pursuant to Article 12(3-b) of the ETS Directive. Emissions from the activities within both the ports of Madeira and Lisbon would benefit from the ETS surrender derogation in this example, as such activities within port are in relation to the voyage Madeira-Lisbon.

To reduce the risk of evasion by container ships and the risk of relocation of container transhipment activities outside the EEA, the EU ETS includes a mitigation measure. According to that measure, stops by container ships at ‘neighbouring container transhipment ports’ do not count to determine the start or the end of a voyage covered by the EU ETS.

The European Parliament and the Council empowered the Commission to adopt implementing acts identifying the ‘neighbouring container transhipment ports’.

A port is to be identified as a ‘neighbouring container transhipment port’ when this port meets three criteria set out in the ETS Directive: its share of transhipment of containers exceeds 65% of its total container traffic during the most recent 12-month period for which data is available; the port is located outside the Union but less than 300 nautical miles from a port under the jurisdiction of an EU Member State; the country of this port does not effectively apply measures equivalent to the ETS for that port.

The Commission adopted an Implementing Regulation on 26 October 2023, which identifies Tanger Med (Morocco) and East Port Said (Egypt) as ‘neighbouring container transhipment ports’.

This implementing act will be revised every two years.

The European Commission will ensure consistency in the way biomass and renewable fuels of non-biological origin (RFNBOs) and recycled carbon fuels (RCFs) are treated under the different ETS sectors. Hence, the compliance obligations for the use of such fuels are the same in all sectors covered by the ETS, including aviation and maritime.

Currently, emissions resulting from the combustion of sustainable biomass compliant with the sustainability criteria established by the Renewable Energy Directive have a CO2emission factor of zero under the ETS. The exact treatment of RFNBOs and RCFs remains to be determined by the implementing legislation to be developed pursuant to Article 14 of the EU ETS Directive. Adoption of such acts is expected in the course of 2024.

Under the ETS Directive, only half of the emissions from extra-EU voyages are subject to surrender obligations and monitoring must be done on a per voyage-basis. Therefore, half of the fuel mass consumed for each type of fuel should be considered for the calculation of emissions related to an extra-EU voyage.

Yes, the EU ETS Directive provides specific provisions with regards to CCU/S technologies. Companies must not surrender allowances for the following:

- CO2 captured and transferred to an installation to be stored in a storage site in accordance with the CCS Directive;

- CO2 utilised to become permanently chemically bound in a product so that it doesn’t enter the atmosphere (subject to the conditions to be set out in the implementing acts under development; adoption is expected in the course of 2024).

A Step-by-Step approach for Shipping companies

Step 1: Understand the new requirements and adapt your contract(s)

For related implementing and delegated acts, please refer to the section ‘Legislative process’ on CLIMA’s maritime webpage which presents the latest state of play (regularly updated).

No. Relevant stakeholders will have the flexibility to draft clauses with regards to the transfer of costs arising from the surrendering of EU ETS allowances, subject to applicable laws.

(See questions on ‘Shipping companies and operators’ for more information)

Yes. The Commission and the European Maritime Safety Agency (EMSA) are available to answer any queries from stakeholders in relation to the new requirements under the revised MRV Maritime Regulation and the EU ETS Directive. Please contact fitfor55emsa [dot] europa [dot] eu (fitfor55[at]emsa[dot]europa[dot]eu) for any question you may have.

Step 2: Find out which administering authority is responsible for your company

[See questions on ‘Administering authorities’ for more information]

Step 3: Open an account in the Union Registry

[See questions on ‘Buying allowances and surrendering allowances’ for more information]

Step 4: Update the ship’s monitoring plan and submit it to the verifier and the administering authority

Shipping companies will need to submit a monitoring plan for each of their ships falling within the scope of the MRV Maritime Regulation and the ETS Directive to their administering authority by 1 April 2024. By that date, the monitoring plan must have already been assessed as being in conformity with the MRV Maritime Regulation by an independent accredited verifier.

For a ship that falls within the scope of the MRV Maritime Regulation and ETS Directive for the first time after 1 January 2024, the shipping company must submit the monitoring plan to the administering authority within three months after the ship’s first port of call in a port under the jurisdiction of a Member State. The monitoring plan that is submitted to the administering authority must have already been assessed as being in conformity with the MRV Maritime Regulation by an independent accredited verifier.

The monitoring plan should follow updated templates that have been adopted by the Commission. These updated templates reflect the revisions brought to the MRV Maritime Regulation, regarding in particular the inclusion of CH4 and N2O emissions within the scope of that Regulation.

The monitoring plans, in accordance with the revised MRV Regulation, will now be mandatorily submitted through THETIS-MRV. It can be done either by filling in the online form (that will be deployed as of January 2024) or by uploading files in accordance with the new template and IT format (that is available in the FAQ of THETIS-MRV).

Yes. The monitoring plan should be submitted by companies through THETIS-MRV. Verifiers will also need to use THETIS-MRV to conclude on the assessment of monitoring plans sent to them. The submission and approval of monitoring plans by administering authorities will also be done through THETIS-MRV.

Accredited verifiers should be able to perform all verification activities falling under the scope of the MRV Maritime Regulation (i.e., including the verification of emissions reports, aggregated emissions data at company level and assessment of monitoring plans). The accreditation should be granted by national accreditation bodies.

Step 5: Monitor your greenhouse gas emissions

As of 1 January 2024, shipping companies should monitor their emissions in accordance with the revised monitoring plan that should be assessed by verifiers and approved by the administering authority.

Step 6: Prepare your emissions reports and the report at company level and get them verified

Once per year, companies must submit an emissions report for each of the ships under their responsibility, as well an emissions report at the company level (aggregating the data to be reported for ETS purposes). For this purpose, companies must follow the corresponding templates. All ship-level and company-level emissions reports must be verified by an accredited verifier by 31 March of the following year (or by 28 February if requested by the administering authority responsible).

Step 7: Surrender EU allowances

Once aggregated emissions data at company level have been verified and submitted to the administering authority, companies must surrender the equivalent number of allowances in the Union Registry by 30 September of that year.